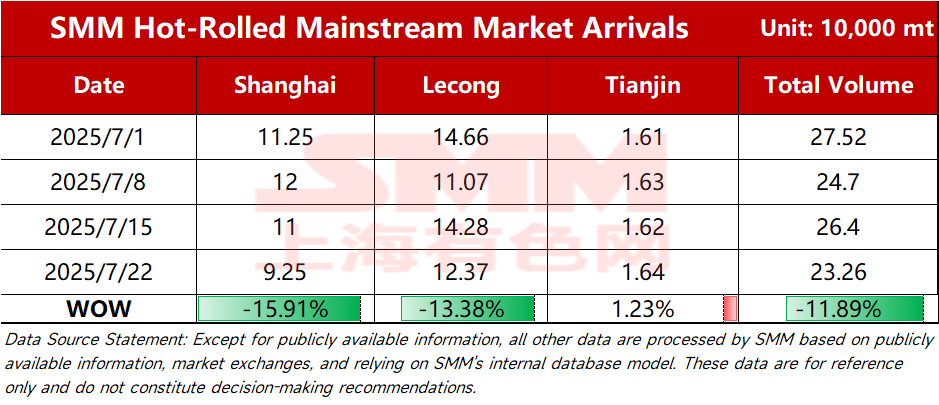

SMM Steel News on July 21: According to SMM statistics, the estimated total shipments of resources in major markets this week were 232,600 mt, a decrease of 31,400 mt from the shipment level WoW. By market:

Chart-1: Comparison of Arrivals in Major Markets

Source: SMM Steel

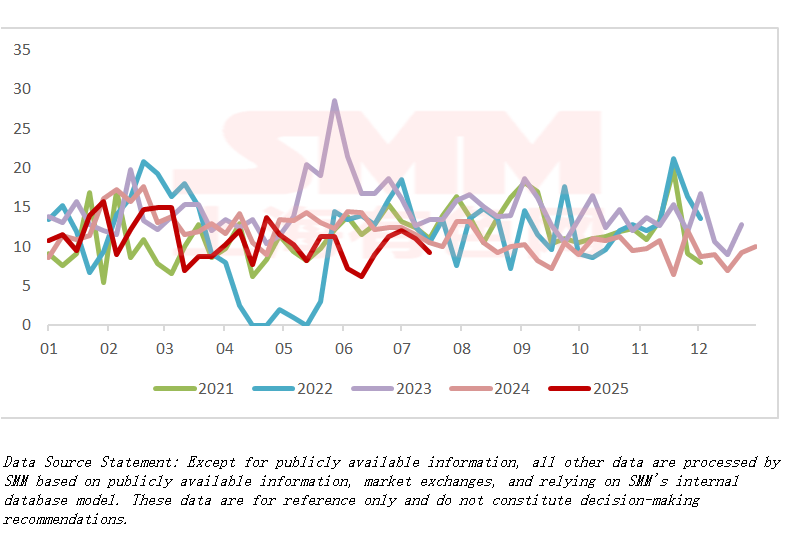

Shanghai Market: Shipments in the Shanghai market declined WoW this week. Specifically, shipments of mainstream resources from north-east and south China decreased, while shipments from north China increased. Looking ahead, with the recent increase in HRC prices, merchants' enthusiasm for ordering has increased, and shipments to Shanghai are expected to increase slightly next week.

Chart-2: Arrivals in the Shanghai Market

Source: SMM Steel

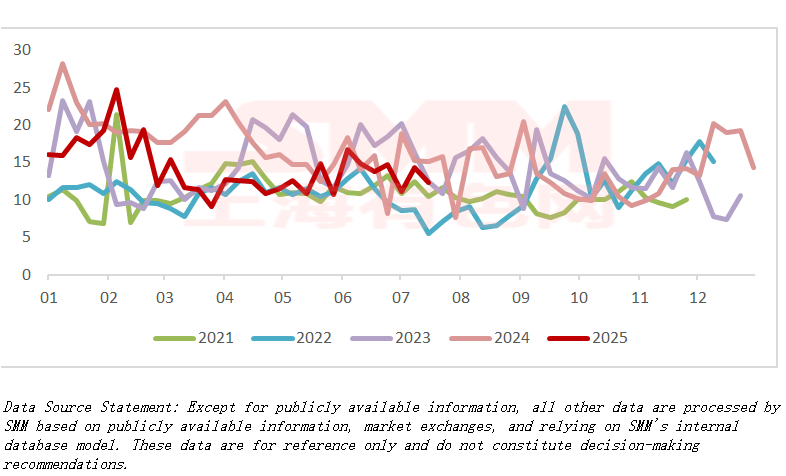

Lecong Market: Shipments to Lecong declined WoW this week. Specifically, on the one hand, arrivals of resources from north China remained stable. On the other hand, due to the price advantage in east China, shipments of local mainstream resources WG and DDH were diverted, resulting in a slight decrease in overall arrivals this week. Looking ahead, with the recent significant increase in spot prices in Lecong and a narrowing of price spreads, it is expected that the short-term arrival level in Lecong will remain moderate.

Chart-3: Arrivals in the Lecong Market

Source: SMM Steel

*This report is an original work and/or a compiled work of SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"). SMM legally owns the copyright and is protected by laws and regulations such as the Copyright Law of the People's Republic of China and applicable international treaties. Without written permission, no one may reprint, modify, sell, transfer, display, translate, compile, disseminate, or disclose the above content to any third party in any other form or permit any third party to use it. Otherwise, once discovered, SMM will pursue legal liability for infringement, including but not limited to demanding liability for breach of contract, returning unjust enrichment, and compensating for direct and indirect economic losses.

The content contained in this report, including but not limited to any or all information such as news, articles, data, charts, images, sounds, videos, logos, advertisements, trademarks, trade names, domain names, and layout designs, is protected by laws related to copyright, trademark rights, domain name rights, commercial data information property rights, and other rights under laws and regulations such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties. It is owned or held by SMM and its relevant right holders. Without written permission, no institution or individual may reprint, modify, use, sell, transfer, display, translate, compile, disseminate, or disclose the above content to any third party in any other form or permit any third party to use it. Otherwise, once discovered, SMM will pursue legal liability for infringement, including but not limited to demanding liability for breach of contract, returning unjust enrichment, and compensating for direct and indirect economic losses. The opinions in this report are based on information collected from the market and the comprehensive assessment of SMM's research team. The information provided in the report is for reference only, and the risks are borne by the user. This report does not constitute direct advice for investment research decisions. Clients should make cautious decisions and not rely on this report to replace their own independent judgment. Any decisions made by clients are unrelated to SMM. In addition, SMM is not responsible for any related losses and liabilities arising from unauthorized and illegal use of the opinions in this report. SMM (Shanghai Metals Market) reserves the right to modify and interpret the terms of this statement.

SMM releases data on HRC shipments to major markets every Tuesday. To subscribe or follow more data, please scan the QR code below.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)